Finding out you have a lower credit score than expected is not what anyone wants to hear. Especially for those looking to make certain investments, their credit score can easily make or break their opportunity to leverage their money. Maintaining a good credit score provides consumers with access to better loan terms, investment opportunities, and in some industries. The good thing is that learning how to improve your credit score is possible. If you are looking for different ways to improve your credit score, here is what truly matters.

How Credit Scores Are Calculated and How to Improve Yours

In the United States, various models are used to review and calculate your credit score, with two of the most popular models being FICO and VantageScore. These models collect and review information from different lenders, then calculate a credit score based on the information found in the report.

Since there are multiple models calculating credit scores, there may be a slight variation in your score if you were to compare the reports from each agency. Consumers often notice a discrepancy between numbers, sometimes varying by as much as 10 points.

The methods used to calculate credit scores may vary depending on the information used, the model employed, and the date the score was calculated. All of these factors both positively and negatively impact your credit score.

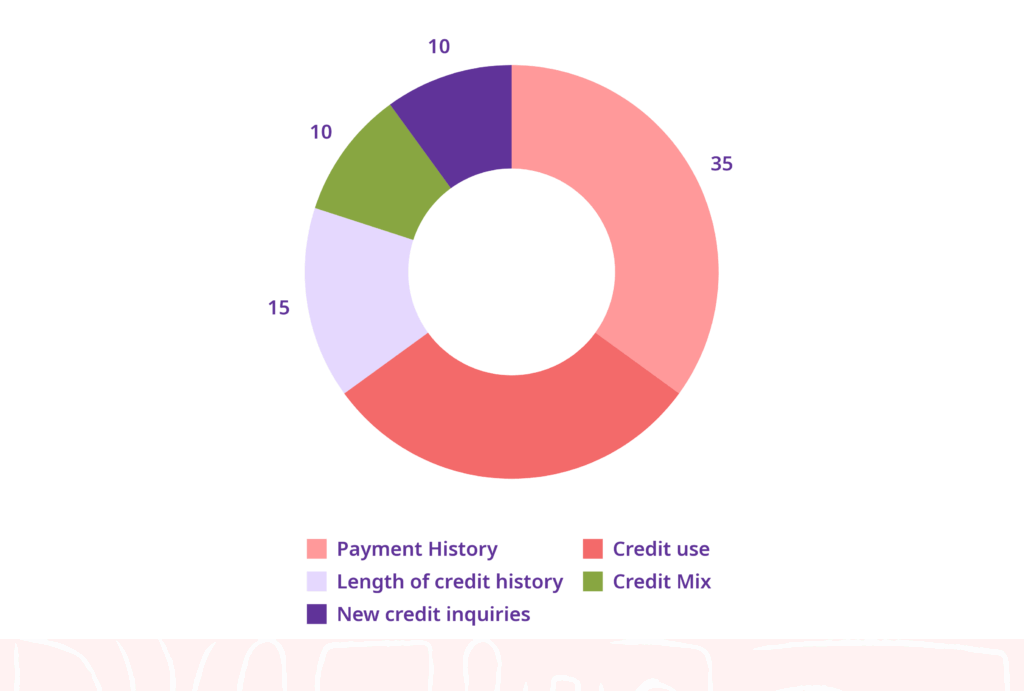

Credit scores are determined by data from these five different areas:

- Payment History (35%)

- Credit use (30%)

- Length of credit history (15%)

- Credit Mix (10%)

- New credit inquiries (10%)

Once they are calculated, the reports are then presented by three major credit-reporting agencies, called Experian, TransUnion, and Equifax.

For more information on how to obtain a copy of your credit report, visit USA.gov/credit-reports.

How to Improve Your Credit Score by Paying Bills on Time

A missed payment in your credit history can make a serious dent in your final score. Your payment history is the most significant factor, accounting for 35% of your total credit score.

For some consumers, even one mistake on their payment history can affect them for many years.

A credit history report typically shows the last seven years of credit use. It shows all the payments you have made and whether you have consistently met the terms of your agreements with lenders. This means that missing a payment is also reported, and a missed payment will appear on your credit report from the moment your account becomes delinquent or about 30 days after the missed payment.

It is important to note that some companies may offer to “fix” your credit for a fee; however, according to the Consumer Financial Protection Bureau, there is no way to remove negative information from a credit report.

Improve Your Credit Score by Lowering Credit Utilization

The credit utilization rate (or ratio) is a percentage of your total available credit that you’re using. For example, you may have a total available credit of $75,000, but you only have $2,000 in credit card debt. That means you’re using only 2% of your credit.

NerdWallet breaks down how to calculate your credit utilization ratio:

- Add all your debts

- Add all your credit limits

- Divide the total outstanding balance by the total credit limit

- Finally, multiply by 100 to get the percentage rate.

If you do not want to do the math, there are many online calculators to help you determine your Credit Utilization Ratio.

How to Calculate Credit Utilization and Improve Credit Score

Ideally, the credit utilization rate should be kept under 30%, as it is a major component used in calculating your credit score. Agencies weigh this factor as 30% of your score. To avoid any negative impact on their credit scores, consumers should pay their credit card bills on time and in full whenever possible. Another way to bypass this is by requesting a credit limit increase from your creditors. Increasing your credit limit will help you maintain a higher buffer, which is necessary to meet the 30% credit utilization ratio.

Why Keeping Old Accounts Open Helps Improve Your Credit Score

Account history makes up about 15% of your calculated credit score. The longer you keep your oldest account open, the better it is for your score. Keeping an old account open may also help improve your credit utilization rate.

Bankrate explains that as time passes and you show your lender that you can make timely payments and use your credit responsibly, they may increase your credit limit for that card. These credit limit increases do not impact your credit score, as they do not involve credit inquiries. You may also request a credit limit increase; however, this will temporarily affect your credit score.

Tips to Keep Old Accounts Active and Boost Your Credit Score

It is recommended that consumers periodically use an old credit card for small transactions, such as those at a fast-food restaurant or their favorite coffee shop, and pay the amount owed as soon as possible. To keep the credit card account active, users should make these minor transactions every couple of months.

How to Improve Your Credit Score by Fixing Credit Report Errors

While unlikely, there is a chance that an error appears on your credit report. The best way to check is by requesting your report and reviewing what accounts were reported. Once you identify the error, you may submit a formal dispute with a detailed explanation and copies of any documents supporting your claim (you can download the template from the Federal Trade Commission).

All disputes must be submitted directly to the credit reporting agency, either online or by mail. No matter the credit reporting agency from which you obtained your report, the agency’s contact information should be readily available for your use. It is also advised to send a copy of your dispute to the provider who reported the error.

After all documents are submitted, the credit agency will conduct an investigation and present the results within 30 to 45 days.

Final Tips on How to Improve Your Credit Score the Right Way

A good credit score is necessary to make large purchases, such as buying a car or a house. But if you don’t pay your bills on time, lower your credit use, or keep older accounts open, your score may take a hit.

Consumers who consistently follow these tips will find that their scores gradually improve over time. Building these habits will benefit them in the long run, particularly when making investments or considering opening another credit line.