A good credit score can be the difference between one’s ability to buy a new car, receive approval for a personal loan, and even qualify for that flashy platinum travel credit card. But did you know that credit scores also play a crucial role in determining the interest rate offered when applying for a home loan? Credit score and mortgage rates are intertwined like peanut butter and jelly on a dream house sandwich.

If you are considering buying a house soon and are curious to learn how interest rates can impact your ability to secure a reasonable mortgage rate, here is what you need to know.

What Is a Credit Score and Why It Impacts Mortgage Rates

The Consumer Financial Protection Bureau states that a credit score is an estimate of your ability to pay off debt on time. Your credit score will fall somewhere between the numbers ranging from 300 to 850, with 300 being the lowest possible score and 850 being the highest possible score. Consumers should try to maintain high scores by practicing good financial habits.

How Credit Scores Are Calculated and Affect Mortgage Rates

There are three major credit-reporting agencies in the United States, each collecting and maintaining consumer credit information from different models (FICO or VantageScore). These three agencies are called: Experian, TransUnion, and Equifax.

Since there are multiple models calculating credit scores, there may be a slight variation in your score if you were to receive the report from each agency and compare them side by side. In fact, consumers often notice a discrepancy between numbers, sometimes varying by as much as 10 points.

The methods used to calculate credit scores may vary depending on the information used (and excluded), the model employed, and the date your score was calculated. All of these factors can both positively and negatively impact your credit score.

How Lenders Calculate Credit Scores and Set Mortgage Rates

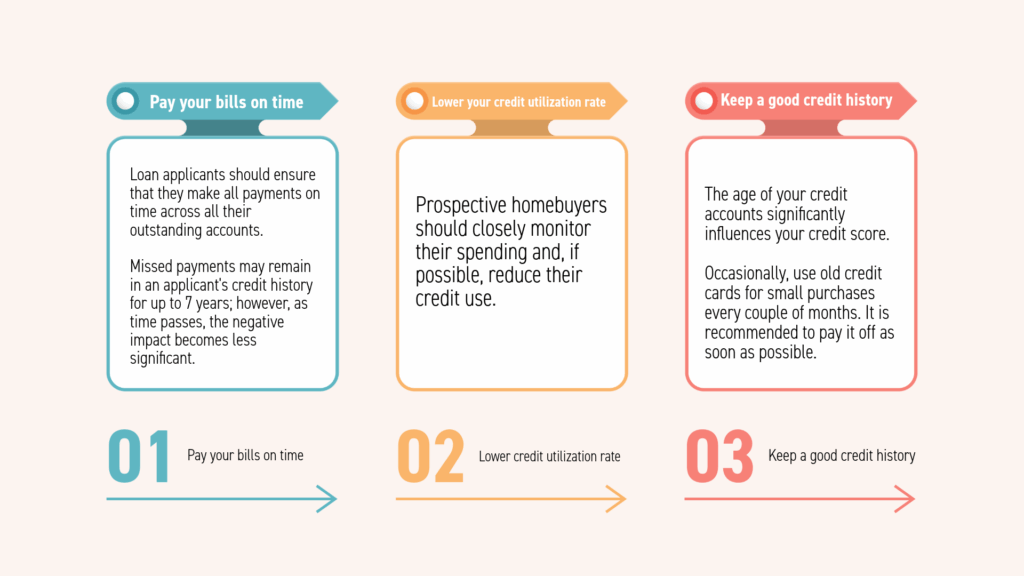

- Payment history – Proof that you have paid your bills on time, including car payments, credit cards, personal loans, and mortgages.

- Total amount owed – A total of all your outstanding debt, including credit cards, personal loans, car payments, and any existing mortgages. This total also determines your debt-to-income ratio, for which a lower ratio is generally preferred.

- Length of credit history – Generally, the longer the credit history, the better it is for your credit score. Older adults with good financial health tend to have higher credit scores than others.

- Credit mix – Lenders prefer to see different types of credit in your history, from car payments to personal loans and credit cards. A healthy financial profile will display various types of debt across different types of loans.

- New credit – Lenders want to see how often you apply for new credit. This check does not include automatic credit limit increases that banks sometimes apply to your credit limit.

For more information on how to obtain a copy of your credit report, visit USA.gov/credit-reports.

How Lenders Use Credit Scores to Set Mortgage Rates

Your credit score can make or break your ability to qualify for a mortgage. When you apply for a home loan, lenders review an applicant’s credit score, alongside other financial information on their profile.

Having a high credit score tells lenders that you are a lower-risk applicant, which usually secures a lower interest rate, reduces the rate of your Private Mortgage Insurance payment, reduces the need for discount points, and minimizes upfront costs. Similarly, consumers with a low credit score are considered to be a higher risk. As a result, lenders may refuse a loan to the consumer or may offer a higher interest rate to help offset their risk.

Credit Score and Mortgage Rates Explained by Score Range

- 620 and below – Buyers will not qualify for a conventional loan, but may look at other loan programs such as the VA, FHA, or USDA to be eligible for a home loan. Despite these alternative programs, applicants will still have to pay higher interest rates, resulting in increased monthly payments.

Monthly Payment Example: Credit Score and Mortgage Rates Compared

Loan applicants with higher credit scores usually save thousands of dollars over the lifetime of their home loan when compared to other applicants. Below is an example explaining how savings are possible:

Let’s say two buyers each apply for a $300,000 home loan. Buyer A has a score of 760, while Buyer B has a score of 640. According to FICO data (one of the data models used to calculate credit scores), Buyer A could qualify for a rate more than 1% lower than Buyer B, saving about $200 per month, or $72,000 over the lifetime of the loan.

Important: The example above is for educational purposes and does not represent an actual mortgage rate quote. Mortgage rates vary based on lender, credit profile, and market conditions. Questions about credit scores should be discussed with a licensed mortgage professional.

Tips to Improve Credit Score Before Applying for a Mortgage

Prospective homebuyers should consider increasing their credit scores as soon as they begin saving to buy a house, with the understanding that debt takes time to pay off and scores also require time to improve.

Here are some tips to help increase your credit score:

Why Credit Score and Mortgage Rates Matter When Buying a Home

Prospective homebuyers should aim to have a credit score as close to 850 as possible. A good credit score can help reduce interest rates, leading to better loan terms and potentially thousands of dollars in savings throughout the life of the loan. Prospective home loan applicants looking to improve their credit scores can do so by paying off debt, making consistent credit card payments, and maintaining a credit card history that is free of late or missed payments.